Finro analyzed 156 AI acquisitions across 14 niches in Q2 2026, and the data tells a story that contradicts conventional founder wisdom: bigger exits don't equal better multiples. In fact, the math shows something most owner-operators miss when planning their exit strategy.

The Capital Efficiency Paradox

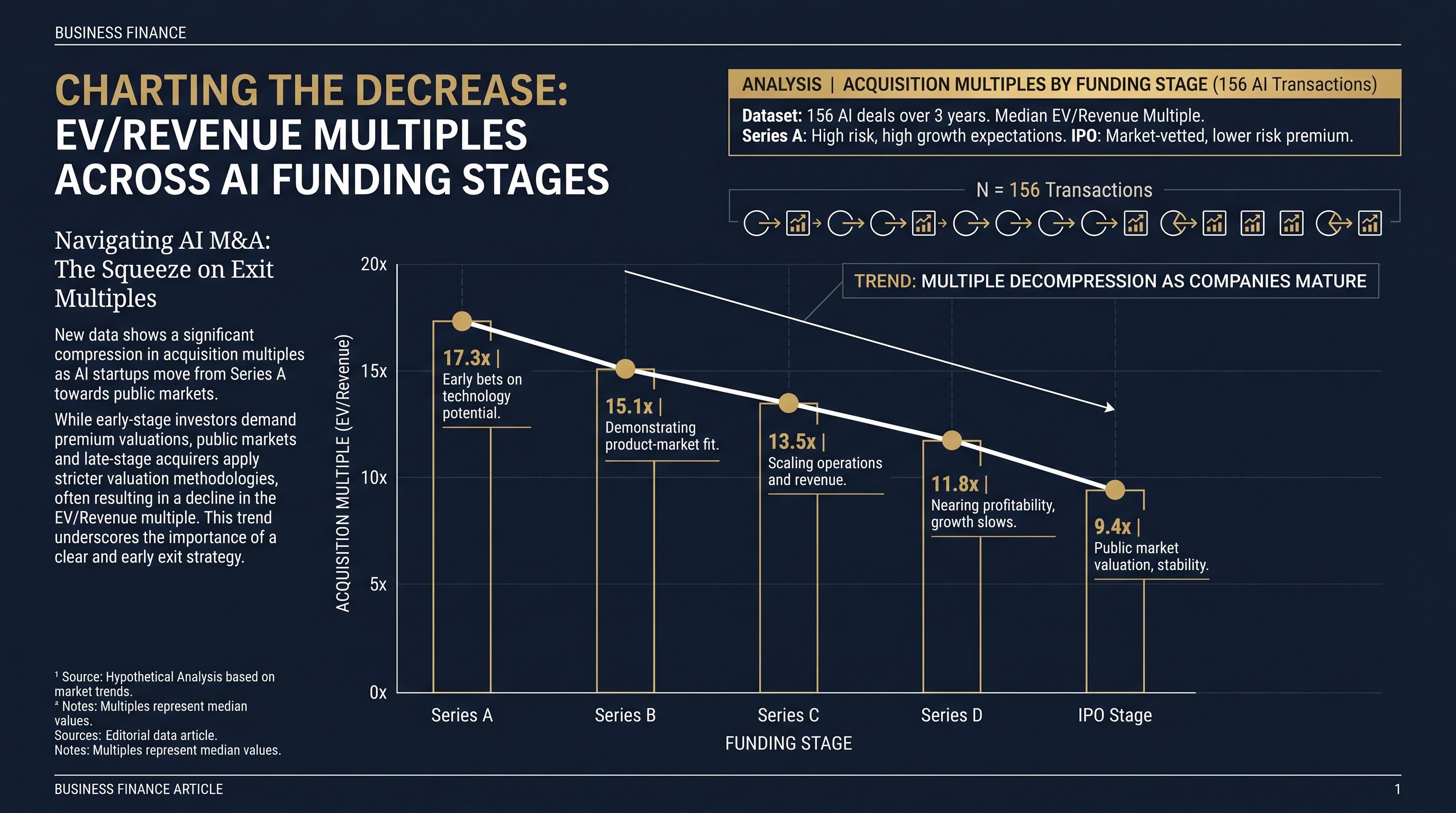

Series A companies reached 17.3x EV/Revenue multiples in Q2 2026. Compare that to the data below, and the pattern becomes clear. Capital efficiency peaks early. Seed-stage acquisitions showed 12x EV/Revenue; Series C companies dropped to a median of 5.7x EV/Funding. The largest exits, the unicorn acquisitions that grab headlines, rarely fetch premium multiples on the capital raised.

Salesforce's $3.6B acquisition of Fin in June 2026 exemplifies this. A large absolute exit value, yes. But the multiple tells the real story: a company that had raised capital across multiple rounds, evaluated against a revenue or funding baseline, didn't command the same relative premium that an earlier-stage exit would have.

The Finro dataset breaks this down by stage:

| Funding Stage | EV/Revenue Multiple | EV/Funding Multiple | |---|---|---| | Seed | 12.0x | 1.9x | | Series A | 17.3x | 6.1x | | Series B | — | 4.7x | | Series C | — | 5.7x | | Public/IPO | 9.4x | , |

What this table reveals: Series A companies achieve the peak EV/Revenue multiple at 17.3x. They have operational traction. They have institutional validation. They haven't yet raised so much capital that the exit value gets diluted across funding rounds. Series B and Series C follow a downward trend on EV/Funding multiples. The company that raises a $10M Series B and then exits at $100M has a 10x exit, which sounds impressive until you realize a Series A company exiting at $50M after raising $8M totals a 6.25x multiple on capital.

The larger picture from Finro's 14-niche analysis: infrastructure, data intelligence, cybersecurity, health tech, legal tech, HR tech, marketing tech, computer vision, fintech, and productivity tools all follow the same pattern. Capital raised after Series A rarely compounds in proportion to what acquirers will pay.

What Acquirers Actually Value

The strategic buyer isn't buying your runway. They're buying the systems, the repeatable processes, and the transferability of your business model. At Angel Investors Network, I've watched hundreds of founders negotiate exits. The ones who got premium multiples all had the same thing: documented, repeatable systems that worked without them in the room. That's not a nice-to-have. That's the entire valuation thesis.

An acquirer's diligence checklist centers on three questions:

- Does this business run on systems or on the founder?

- Can the revenue continue without the CEO making every key decision?

- Are the customer relationships proprietary, or are they tied to a person?

The Series A companies hitting 17.3x multiples had answers to all three. They had moved beyond founder-led sales. They had documented playbooks. They had customer contracts that outlasted handshake agreements. That's why they commanded premium multiples while still being small enough to be acquired quickly, before the cost of integration became prohibitive.

Compare this to the BlueConic acquisition of Blueshift, a martech consolidation play in the same quarter. The acquirer was buying a team, a technology, and a customer base. But the multiple? Martech acquisitions in Q2 2026 averaged 4.8x EV/Revenue for Series B and later. Early-stage martech achieved 18.2x. The difference was transferability.

The Owner's Exit Engine Framework

Building an acquirable business requires thinking about exit math from day one. The Owner's Exit Engine framework maps to what acquirers measure:

- Foundation: Systems must exist independent of the founder. Documentation, SOPs, playbooks, recurring revenue contracts.

- Validation: Market proof. Revenue growth that doesn't depend on the CEO doing the selling. Gross margins above 70% signal product-market fit.

- De-risking: Customer concentration below 30% from any single customer. Recurring revenue as a percentage of total revenue. Churn rates below 5% monthly.

Companies that build these three layers by Series A exit at premium multiples. Companies that add Series B and Series C capital but don't scale these layers proportionally see multiples compress. The math is unforgiving.

The UK M&A market in Q1 2026 showed similar patterns. According to Moore KS research, 54% of deals involved private equity, and of tech-led acquisitions, 70% were martech. PE buyers specifically target companies with repeatable, scalable unit economics because they're buying the ability to apply the same playbook across portfolio companies. That's where premium multiples attach.

The Capital Efficiency Ceiling

Finro's data shows that after Series A, each additional funding round compresses the EV/Funding multiple. Series B companies at 4.7x, Series C at 5.7x. This isn't because later-stage companies are worth less; it's that acquirers don't proportionally value each new dollar raised. A Series A company with $8M raised and $10M ARR hits the sweet spot. A Series C with $50M raised and $15M ARR is a harder sell relative to the capital consumed.

The doctrine here is direct: legacy matters more than lifestyle. A founder who raises enough to build the business but not so much that venture return expectations become impossible is building a legacy. A founder who pursues large Series B and C rounds because the metrics look good on paper is often building a trap. The exit multiple won't cover the capital weighted across all rounds. The multiple compresses. The founder's eventual equity stake gets diluted below what it would have been with disciplined capital raises.

This applies even to the largest exits. The companies exiting at $500M+ rarely achieved those multiples on any single funding round metric. They achieved them by:

- Reaching profitability before exit.

- Building owner-friendly cap tables early.

- Remaining disciplined on capital raises relative to revenue milestones.

FAQ: Exit Multiples for Owner-Operators

Q: If Series A hits 17.3x EV/Revenue, should I try to exit at Series A?

A: Not necessarily. The 17.3x is a median across 156 deals, and the range is wide. A Series A company exiting at 3x revenue exists alongside one exiting at 30x. The multiple depends on niche, growth rate, and gross margins. But the principle holds: raising more capital after you hit product-market fit doesn't proportionally increase exit value. Focus on profitability and recurring revenue, not the next round size.

Q: How do I know if my business has the systems an acquirer wants?

A: Run The Owner's Exit Engine audit. Document your top 20 business processes. Which ones require you personally? Which ones have written procedures that a new hire could follow? Which revenue streams could operate for 90 days without your involvement? If the answer to the third question is "almost all of them," you have acquirable systems. If it's "none," that's your first project, not your exit.

Q: Salesforce paid $3.6B for Fin. Why doesn't that company have a 17.3x multiple?

A: Because $3.6B is an absolute exit value, not a multiple. Fin likely raised $200M+ across multiple rounds. The multiple on total capital deployed is lower than a smaller Series A exit because larger capital bases compress multiples. Salesforce is buying a strategic asset and a team. Smaller acquirers in the 156-deal dataset are buying businesses that can operate independently and be integrated quickly. Different criteria, different multiples.

Q: Is the 4.7x EV/Funding multiple for Series B a warning sign?

A: It's a signal to be intentional. If you're raising Series B, it should be to accelerate a bottleneck, not to extend runway or fund new experiments. A Series B that doesn't visibly improve product velocity, gross margins, or market expansion is destroying multiple. Acquirers see $15M ARR after a $20M Series B and ask why you needed the capital. Answer that question before you raise.

Q: Which niche has the highest exit multiples?

A: Infrastructure and data intelligence rank highest across the Finro dataset. Infrastructure especially because it's more difficult to build and creates switching costs. But within any niche, systems and transferability matter more than category. A well-built martech company at 14x exits higher than a poorly-built infrastructure play at 8x.

The Numbers Don't Lie

The Finro dataset of 156 acquisitions is the most granular view of Q2 2026 M&A available. Read it. Understand where your business stages in terms of funding, revenue, and niche. Then read the analysis on sell-side auction vs. broker exits to see how you'll be sold. Finally, study how a $400M agentic GTM company achieved PE acquisition multiples to see what happens when systems, growth, and de-risking align.

The path to a premium multiple isn't mysterious. It's documented in exit data. It follows repeatable patterns. Capital efficiency peaks at Series A not by accident but by design: that's when a business has proven product-market fit without yet carrying the burden of excessive capital. Series B and later can work, but only if you raise capital in proportion to new revenue created.

Your exit number isn't set by ambition. It's set by the multiple your business qualifies for at the moment you exit. Build the systems first. Raise capital second. Exit when the multiple exceeds the cost of staying independent.

Legacy matters more than lifestyle. The data proves it.