Vista Paid a SaaS Multiple for Nexthink. Then AI Revenue Hit $109M.

TL;DR:

- Vista Equity Partners acquired Nexthink in March 2026 at a SaaS multiple, after tracking the company for six years.

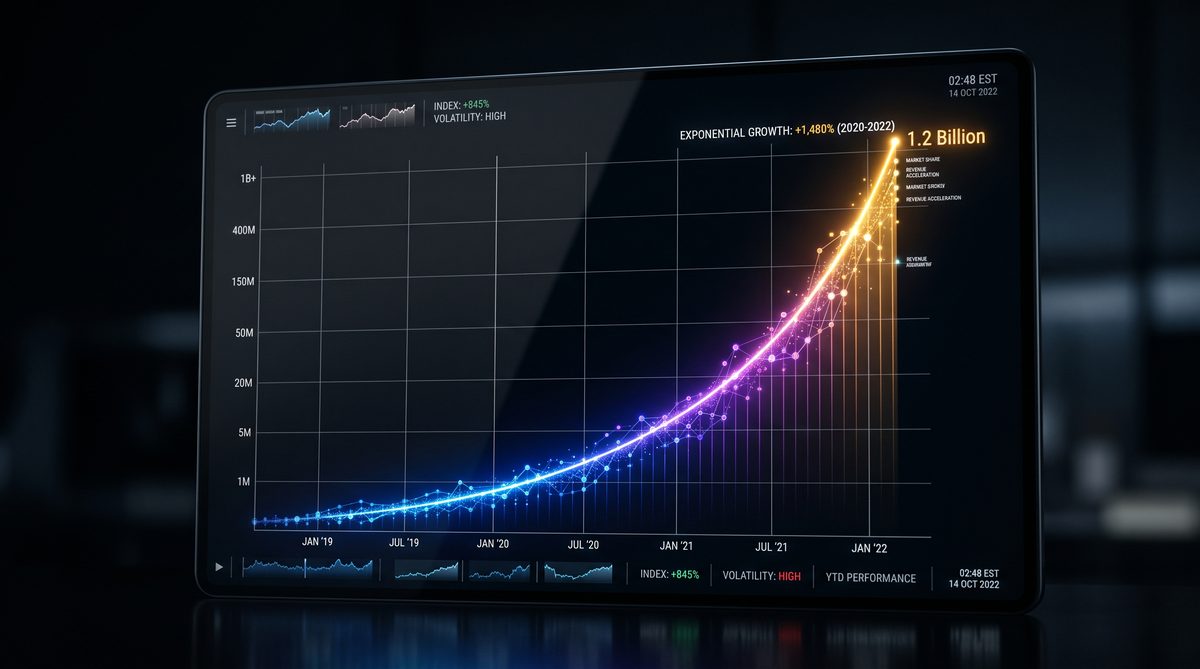

- Nexthink's AI-native recurring revenue grew from $20 million to $109 million in twelve months, roughly 5.5x, and is projected to exceed $200 million within two years.

- The founder built the AI layer before the buyer showed up. Vista priced the SaaS business. The market is now pricing the AI layer for them.

Vista Equity Partners bought Nexthink at a SaaS multiple, not an AI multiple, then watched the company's AI-native revenue grow more than five times in a single year. That is not a rounding error. It is the gap between what a buyer pays for a recurring-revenue asset and what the same asset becomes once the AI layer compounds past the point where anyone can still call it plain software. Source: Vista Equity Partners

Nexthink sells digital employee experience software. IT teams use it to see what is breaking across laptops, apps, and networks before employees notice. Vista tracked the company for six years before moving. When they finally wrote the check, closing the deal in March 2026, they valued Nexthink at roughly $3 billion, using standard SaaS math.

Vista's own words on the deal are direct. The company was acquired at a SaaS multiple. What it is becoming, the layer that keeps the agentic enterprise functioning, is worth considerably more.

I have stood watch on machinery that looked identical to the manual right up until the moment it wasn't. That is the pattern here. Nexthink looked like a SaaS company on the balance sheet Vista underwrote. It was already becoming something else on the product roadmap nobody had fully priced.

What Actually Happened in the Deal

Permira first invested in Nexthink in March 2021 through a growth equity round. Over four years, the company more than tripled annual recurring revenue, completed its shift to a multi-tenant SaaS platform, and pushed hard into automation and AI. Source: Permira via Capital Riesgo

That is the setup most owner-operators skip. Permira did not just hold the asset and wait. They forced the transition to recurring, multi-tenant infrastructure first. AI got built on top of a system that was already sellable, not bolted onto a legacy platform after the fact.

Vista announced its majority investment in October 2025, valuing Nexthink at approximately $3 billion. Source: Nexthink The deal closed in March 2026 after regulatory approval. Founder and CEO Pedro Bados stayed on to run the company. What changed was who captured the next leg of growth.

Here is the number that matters. Nexthink's flagship AI product, Spark, is an autonomous IT agent that resolves roughly 77 to 80 percent of issues on first contact, in under two minutes, with zero ticket created. The industry average first-contact resolution rate is about 15 percent. Spark runs at five times that. Source: Nexthink

That product barely existed as a shipped, monetized line when Permira first invested in 2021. By the time Vista closed, AI-native recurring revenue had grown from $20 million to $109 million in twelve months. Vista's own projection: north of $200 million within two years, more than half of total company revenue.

The Multiple Gap Is the Whole Story

This is where the math gets uncomfortable for anyone who has not separated their AI revenue from their legacy revenue on paper.

Across 2026 M&A transactions, AI-native software companies commanded a median buyout multiple of roughly 11.5x revenue. Legacy SaaS, the per-seat subscription model without meaningful AI, commanded roughly 3.8x. Source: Ryan Allis, AI Software Valuation Report 2026 That is not a premium. That is a different asset class wearing the same balance sheet.

Vista bought Nexthink at the SaaS number. The company's AI-native line is now compounding toward the AI-native number. Every dollar of that $109 million, and every dollar of the $200 million coming, gets captured by the new owner at the multiple they will command at the next exit, not the multiple Vista paid to get in.

PwC's deal advisory team put it plainly in their 2026 outlook. Companies that command premium exits are the ones using AI to accelerate their own product roadmap, not the ones bolting AI onto a stale core. Source: PwC Product velocity, not margin expansion, separates a premium exit from an average one now.

Think of it as a casualty drill nobody ran in time. The ship takes on water in one compartment, the AI-native revenue line, while the rest of the vessel is still valued as if the whole hull is uniform. The buyer who understands where the compartments are gets to seal them off and price them separately. Most sellers never draw the bulkhead.

The Owner's Exit Engine Framework

I teach owner-operators a structure I call the Owner's Exit Engine. It has four gears, and Nexthink ran all four before Vista ever wrote a check.

Gear one is operator independence. The business has to run without the founder in the room. Nexthink kept Bados in place post-close, which tells you the system, not the founder, was already carrying the operation.

Gear two is the recurring core. Permira forced the multi-tenant SaaS transition years before AI became the story. You cannot bolt AI-native pricing onto a business that still bills like it is 2015.

Gear three is the compounding layer. This is the AI-native product line, priced and tracked separately from legacy revenue, so a buyer can see the growth curve in isolation. Nexthink built Spark, Assist, and Drive as a distinct product suite with its own revenue tag.

Gear four is the receipts. Nexthink did not claim their AI worked. They published a 77 percent first-contact resolution rate against a 15 percent industry baseline, with a two-minute average resolution time. That is the math a buyer can underwrite.

Most founders build gear one and stop. They exit with a sellable business at a SaaS multiple and call it a win. Nexthink built all four gears and let the buyer discover, twelve months into ownership, that gear three was worth more than the whole deal price implied.

The Founder Dependency Tax, Inverted

I have written before about the founder dependency tax, the discount buyers apply when a business cannot run without the person who built it. Nexthink shows the inverse problem. Call it the AI arbitrage tax. It is the discount a buyer captures when the seller has not yet separated and priced their AI-native revenue as its own asset.

That tax gets paid by whoever owns the business when the market finally prices it correctly. In this case, that is Vista, because Vista bought before the market caught up. If Nexthink's leadership had waited another eighteen months and gone to market with $109 million in AI-native ARR already visible, they likely would have negotiated a blended multiple, not a pure SaaS one.

They did not wait. Permira exited. Vista bought the arbitrage. The lesson is not that Nexthink made a mistake, since six years of Vista tracking the deal and a $3 billion valuation is a strong outcome for any founder.

I think about this every time I coach a founder who is three years from a planned exit and still running the business off a founder-shaped bottleneck. The business they will sell in three years is not the business they have today. If they do not build the compounding layer now, the buyer gets to.

What This Means If You Are Building to Sell

The operator lesson here has nothing to do with IT operations software. It is about sequencing.

If you are building a business with any AI-native product line, whether that is an automation layer, a proprietary model, or an agent doing work a human used to do, you need three things in place before you go to market, not after.

First, separate the revenue. If your AI-native product revenue is commingled with legacy subscription revenue on your P&L, no buyer can price the arbitrage, and neither can you. Break it out as its own line with its own growth curve.

Second, publish the receipts. Nexthink did not say Spark was good. They said 77 percent first-contact resolution versus a 15 percent industry average, with sub-two-minute resolution times. Verification beats optimism every time a buyer's diligence team opens your data room.

Third, run the timeline math before you negotiate. Research from Aventis Advisors put median private SaaS M&A multiples at roughly 3.1x revenue in early 2026. Windsor Drake's research shows AI-enabled companies in the same revenue range trading at 7.5x to 14x, depending on depth of AI integration. Source: Qubit Capital That gap is the number you are negotiating against, whether you know it or not.

I learned to run pre-mortems in the Navy, long before I ran them in a boardroom. Before a casualty drill, you walk the compartment and ask what fails first. Before an exit, you walk your revenue lines and ask which one the buyer is about to underprice. If you cannot answer that with receipts, you are the seller giving away the compounding, not the one capturing it.

Doctrine Connection: Competence Beats Credentials

Vista did not buy Nexthink because of a pitch deck or a brand name. They tracked the company for six years and bought based on what the product actually did: an autonomous agent resolving 77 percent of issues on first contact, verified in production, at scale, across real enterprise deployments. That is competence, demonstrated in receipts, beating any credential a founder could have claimed instead. The market rewarded the demonstrated capability with a valuation trajectory the SaaS multiple never captured on day one.

Frequently Asked Questions

Q: What multiple did Vista actually pay for Nexthink? Vista has not disclosed the exact revenue multiple publicly. The deal valued Nexthink at approximately $3 billion, and Vista has stated directly that the price reflected a standard SaaS multiple, not an AI-native premium. Industry data from 2026 puts median SaaS M&A multiples around 3.1x to 3.8x revenue, versus roughly 11.5x for AI-native companies.

Q: How did Nexthink's AI-native revenue grow that fast? The growth came primarily from Spark, an autonomous IT agent that resolves issues without creating a ticket, plus companion products Assist and Drive. Spark's first-contact resolution rate of 77 to 80 percent, against an industry average of 15 percent, drove rapid enterprise adoption once the product launched broadly in early 2026.

Q: Can other owner-operators replicate this arbitrage? Yes, but only if the AI-native revenue is built and tracked before the exit conversation starts. The arbitrage exists because buyers price what they can verify today, not what a product might become. Separate your AI revenue, publish verified results, and negotiate the blended multiple before you sign, not after.

Q: Does this mean Vista overpaid or underpaid for Nexthink? Neither, by the numbers available. Vista paid a fair SaaS-market price for the business as it existed at signing. The AI-native growth that followed was not fully priced into that number, which is exactly what Vista's own public statement acknowledges. The company is worth more today than the price paid, and Vista is now the one holding that upside.

Q: What is the single action step for a founder-operator reading this? Pull your P&L this week and separate any AI-driven or automation-driven revenue line from your legacy recurring revenue. If you cannot make that split cleanly, that is your 90-day project, before you take a single exit meeting.

*Jeff Barnes is the founder of demg.ai and Digital Evolution Marketing Group. This article is educational and does not constitute business, legal, or financial advice. All claims are sourced where possible. Results vary by business, market, and execution.*