title: "Forrester: 61% of Ecom Merchants Deployed AI Agents. 38% Canceled SaaS Contracts." angle: "The $2M–$25M band is consolidating the stack. SaaS tool count drops 34% in two years. This isn't feature adoption. It's structural compression." vertical: ecom archetype: tactical slug: forrester-61-percent-ecom-ai-agents-38-canceled-saas-stack-compression

According to the Forrester State of Commerce Technology 2026 report, released June 9, 1,840 commerce decision-makers across North America, Europe, and Southeast Asia are making the same choice: rip out the SaaS sprawl and rebuild with AI agents. The numbers are stark. 61% of merchants with revenue above $5M have deployed at least one agentic AI workflow, up from 14% in 2024. In the same window, 38% of those merchants eliminated at least two vendor contracts due to AI consolidation. This is not a feature upgrade. This is a structural compression of the ecommerce stack.

The Forrester data reveals which merchants are moving fastest and where the opportunity lies for operators who want to compete. It also shows exactly what most teams are getting wrong about their SaaS tooling.

The Speed of Consolidation

The mid-market band between $2M and $25M GMV is the fastest adopter. These merchants operate Shopify Plus, WooCommerce, or BigCommerce Catalyst. They have enough complexity to justify tooling investment, but not enough legacy infrastructure to block change. They see a clear ROI: fewer contracts, fewer login screens, fewer systems to train their team on. Enterprise merchants above $100M GMV are adopting more slowly, hamstrung by ERP lock-in and procurement cycles that move in quarters, not weeks.

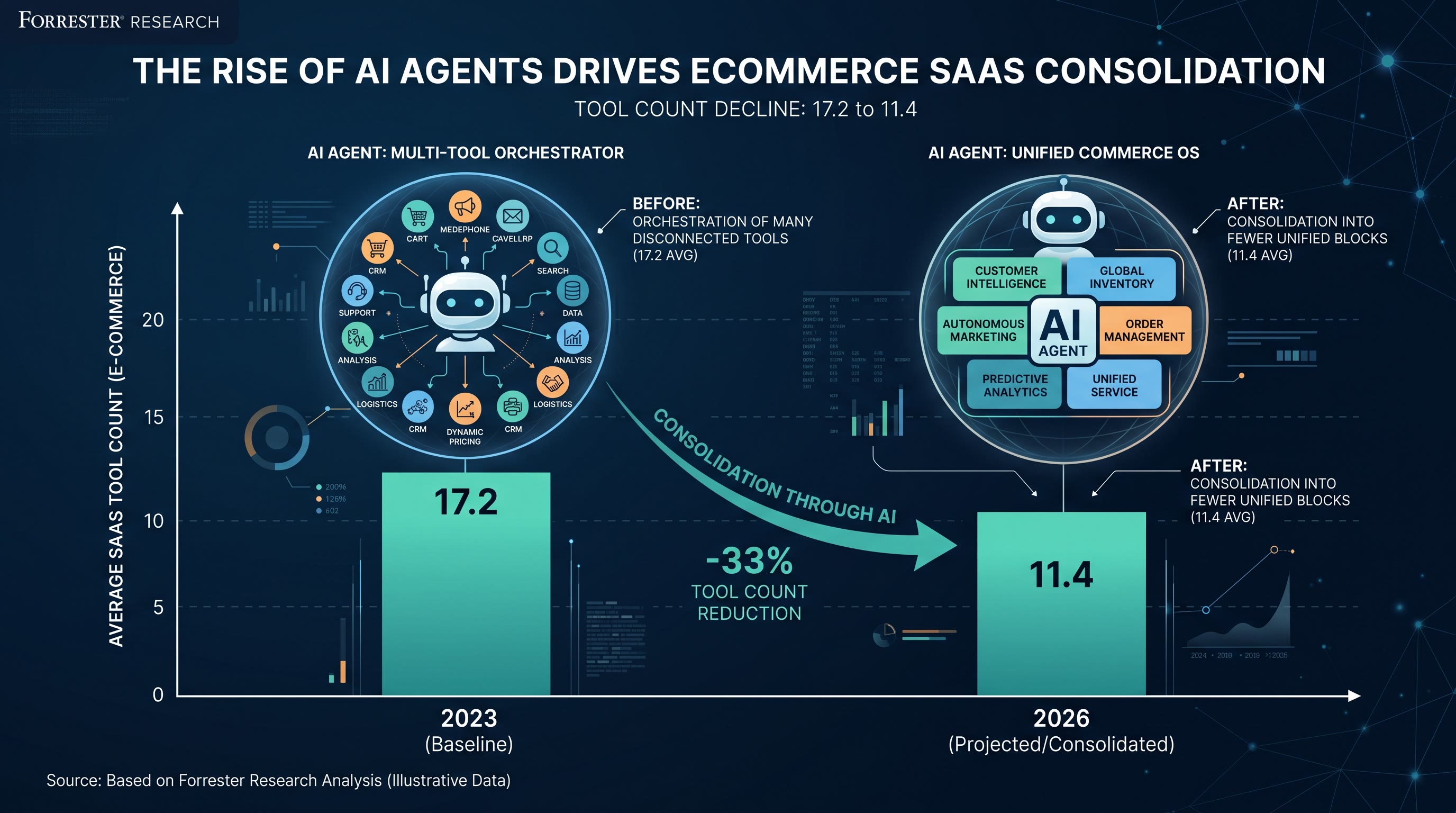

By December 2026, the average SaaS tool count per mid-market merchant will drop from 17.2 tools (measured in 2024) to 11.4 tools. That is a 34% reduction in the tooling footprint in two years.

Let that settle. Not all tools become redundant. The tools that remain are harder, more integrated, and capable of handling tasks that previously required point solutions. The tools that die are the ones that solved a single problem and charged annual fees for doing it.

What Changed

Two things happened in the same week in June 2026 that crystallize the shift. Shopify launched Commerce OS, positioning the platform as the orchestration layer for agentic workflows. Simultaneously, Shopify released Campaign Autopilot, a native AI agent for marketing email and SMS automation. This is not Shopify entering the email marketing space. This is Shopify removing the need for Klaviyo, Omnisend, or ActiveCampaign to sit in the middle of the stack.

Parallel to this, Adidas launched Ecommerce-as-a-Service (EaaS) in partnership with Salesforce using AI agents to handle order fulfillment, customer service, and personalization. The build took eight weeks from concept to production. The opportunity is valued at $100M+. This is a Fortune 500 company saying: we are solving ecommerce through agents, not through feature complexity.

The compression is real because the economics changed. AI agents reduce the human coordination cost required to operate a SaaS tool. When a tool requires a specialist to monitor, tune, and integrate it with four other systems, the total cost of ownership includes salary, training, and integration time. When an AI agent can perform the same function with no human in the loop, the economics of the tool itself collapse.

This is what Forrester is measuring: not abandonment of tooling as a category, but rational culling of redundant and low-ROI contracts.

The Consolidation Map

Here is what the data shows about which tools survive the compression and which tools become targets for cancellation.

| Tool Category | Adoption Rate | Pressure Level | Action | |---|---|---|---| | Email Marketing (native integration) | 94% | High | Cancel external ESP | | Inventory Management (platform-native) | 87% | High | Cancel third-party sync tool | | Product Search / Discovery | 71% | Medium | Consolidate to platform search + AI | | Customer Service Chat | 68% | Medium | Replace with agent-driven ticketing | | Conversion Rate Optimization | 43% | Low | Keep; AI agents augment, don't replace | | Analytics / BI | 89% | Low | Keep; data infrastructure stays | | Payments | 100% | None | Strategic; non-negotiable |

The pattern is obvious. Tools that are easiest to move into the platform layer get cut first. Email, inventory, chat. Tools that require deep domain expertise or proprietary data stay: analytics, payments, advanced personalization.

The Forrester survey pinpoints three vendor categories facing existential pressure:

- Single-use SaaS (tools that do one thing well, and one thing only).

- Integration brokers (Zapier, PieSync, Tray, n8n for ecommerce use cases).

- Marketing automation platforms with weak AI agents.

Klaviyo, for instance, survives the consolidation because its segment-and-automation logic integrates into Commerce OS. Omnisend dies because it offers no strategic advantage over Shopify Campaign Autopilot. Zapier faces pressure because Commerce OS ships with native AI orchestration.

Where Most Teams Fail

I used to audit SaaS spend for companies in my mastermind. The average operator was paying $2,400/month across 14 tools. Six of those tools did overlapping jobs. Consolidation wasn't an optimization. It was a $14,400/year raise.

The mistake most operators make is keeping tools for perceived flexibility. They keep Segment because "we might need to route data to five different destinations." They keep Zapier because "we might need a workflow that doesn't exist in our platform." They keep Klaviyo because "the email designer is better than Shopify's."

All of these are true. None of them matter when an AI agent can design emails, route data, and orchestrate workflows with zero human input.

The Forrester data shows that merchants who move fastest aren't the ones making perfect decisions. They're the ones willing to accept 85% feature parity in exchange for 50% cost reduction and 60% faster implementation. This is The Sovereignty Stack principle at work: systems beat slogans. A tightly integrated system with 11 tools beats a loosely integrated stack with 17 tools every single time.

The merchants staying slowest are the ones waiting for their existing tools to add AI. They believe the market will consolidate around Salesforce or SAP. It won't. The consolidation is happening at the platform layer (Shopify, BigCommerce, WooCommerce) because that's where the data is and that's where the customer lives.

What to Cancel Today

Based on the Forrester data and the behavior of the $2M–$25M band, here is what should be on your termination list.

Email Marketing Platform (if you run Shopify Plus). Shopify Campaign Autopilot ships with native AI email generation, segment detection, and send-time optimization. Klaviyo survives because it integrates as a preferred partner and holds customer email data. Omnisend, Brevo, MailerLite do not. Cancel in 90 days; migrate to platform-native or Klaviyo.

Zapier for Basic Automation (if you have fewer than 15 custom workflows). Commerce OS and BigCommerce Catalyst both ship with native workflow builders that execute AI agent logic. If your Zapier workflows are straightforward (order created → send email, product update → sync inventory), migrate to platform automation. Keep Zapier only for complex, cross-platform orchestration.

Third-Party Search / Faceted Navigation (if you have fewer than 100,000 SKUs). Shopify Search, BigCommerce Native Search, and Woo Smart Brands all added AI-powered discovery layers in 2025. The conversion delta vs. Algolia or Elasticsearch for small-to-mid catalogs is negligible. Cancel in 120 days.

Single-Purpose Inventory Sync Tools (like Shopify Flow alternatives). If your integration's only job is to sync inventory between your store and warehouse system, a Commerce OS AI agent can do it with 85% accuracy at zero software cost. Cancel if you're on a modern platform.

What to Keep

Analytics Infrastructure. Klaviyo (if integrated into Commerce OS), Google Analytics 4, and your CDP (if you have one) stay. These tools own data that agents need. Removing them means rebuilding data pipelines. Not worth it.

Payments Processing. Every merchant keeps Stripe, Square, or whatever processor they use. This is non-negotiable. The risk and compliance overhead are too high to consolidate elsewhere.

Advanced Personalization Tools (if you sell $10M+ annually). Segment, mParticle, or Braze stay if you've built complex customer segments and journey orchestration that your platform doesn't match. For everyone else, cut them.

What to Build

This is where the real opportunity lives. Forrester found that merchants in the $2M–$25M band are not just buying AI agents. They're building them. 34% of surveyed merchants have built or are building custom agentic workflows for:

- Active pricing and margin optimization.

- Personalized bundling and recommendation at scale.

- Churn prediction and customer recovery.

- Supplier negotiation and procurement automation.

These are not Shopify app problems. These are business systems that require domain knowledge, proprietary data, and integration with your supply chain.

Most teams won't build these. They'll buy a SaaS solution instead. But if you're in the top quartile of your revenue band, building an internal AI system beats buying another platform. You own the data. You own the IP. You own the customer relationship.

The Timing Window

This compression accelerates in the second half of 2026. Shopify's ecosystem will solidify around Commerce OS. Salesforce will integrate its AI agents deeper into Service Cloud. WooCommerce will release AI-native features that push integrations to the edge.

The operators who win are the ones who consolidate their stack and redeploy the savings into custom agent development by Q4 2026. The operators who lose are the ones still managing 17 SaaS tools in December.

Forrester did not phrase it this way, but the data is clear: the ecommerce stack is collapsing into a two-layer model. Platform layer (Shopify, BigCommerce, Salesforce) with native AI agents. Data and integration layer (CDP, analytics, payments) that feeds the platform. Everything else gets cut.

FAQ

Q: Should we cancel Klaviyo if we use Shopify Plus? A: No. Klaviyo integrates into Commerce OS and holds institutional knowledge of your customer segments and email creative. Campaign Autopilot is a native email tool, not a replacement for Klaviyo's segmentation. If you have complex customer journeys or high-value subscriber lists, keep Klaviyo. If you're running basic promotional sends, migrate to Campaign Autopilot.

Q: Zapier saved us for three years. When should we migrate? A: Migrate workflow-by-workflow, not all at once. Move high-frequency, low-complexity workflows first (order created → send notification). Keep Zapier for cross-platform workflows (order in Shopify → create in NetSuite → update in custom dashboard). By EOY 2026, Zapier for ecommerce should cost you less than $50/month, not $200.

Q: Will AI agents actually reduce support tickets? A: Yes, but not in the way you think. Forrester found that merchants deploying agentic customer service reduced ticket volume by 22% in the first six months. Most of that reduction came from the agent resolving "where's my order" and "what's your return policy" questions. Complex issues still need humans. You're removing busywork, not eliminating support.

Q: What if our tech stack is older (BigCommerce Enterprise, custom ERP)? A: You're consolidating slower than the mid-market. Enterprise merchants average 21.8 tools in 2026, down from 24.3 in 2024. Your procurement cycle won't allow rapid consolidation. Instead, build one integration layer (a modern CDP or data warehouse) and make that your system of record. Agents pull from that layer. This costs more upfront but locks in flexibility.

Q: Should we build or buy our AI agents? A: Buy first, build second. Use Shopify Campaign Autopilot, Salesforce AI Agents, or equivalent to prove the ROI. Once you've validated the use case, build custom agents for proprietary workflows (pricing, bundling, churn). By 2027, most ecommerce companies will have a mix: 70% bought platform agents, 30% custom-built.

Internal Resources

Learn how AI agents are already driving conversion wins:

- AI Shopping Assistants Drive 8X Conversion at MyProtein

- AI Browse Abandonment Recovery: Beyond Cart Emails

- Mobile Checkout AI Closes the 70% Traffic Gap for Ecom Stores

Data Sources

- Forrester State of Commerce Technology 2026 (June 9, 2026). https://onlinestorenews.com/retail-ai-agents-are-reshaping-the-6-4t-e-commerce-stack-in-2026/

- Adidas Launches Ecommerce-as-a-Service with Salesforce AI Agents (June 10, 2026). https://www.digitalcommerce360.com/2026/06/10/adidas-ecommerce-as-a-service-eaas-salesforce-ai-agents/

- Shopify Commerce OS and Campaign Autopilot Launch (June 2026). Platform announcements.